Planning ahead: How businesses, consumers can respond to economic uncertainty

There was quite a bit of uncertainty at the start of 2025 surrounding U.S. and global policies. Central banks had begun cutting rates in 2024 and economic growth was positive in most developed economies coming into the year, but it was unclear how fast rates would fall and how long growth would stay positive. The hope was that by the end of the first quarter, a lot of the uncertainty would have died down, giving investors a good sense of which major policies would be enacted and what campaign promises would be dropped, leading to a better understanding of where inflation and growth were headed.

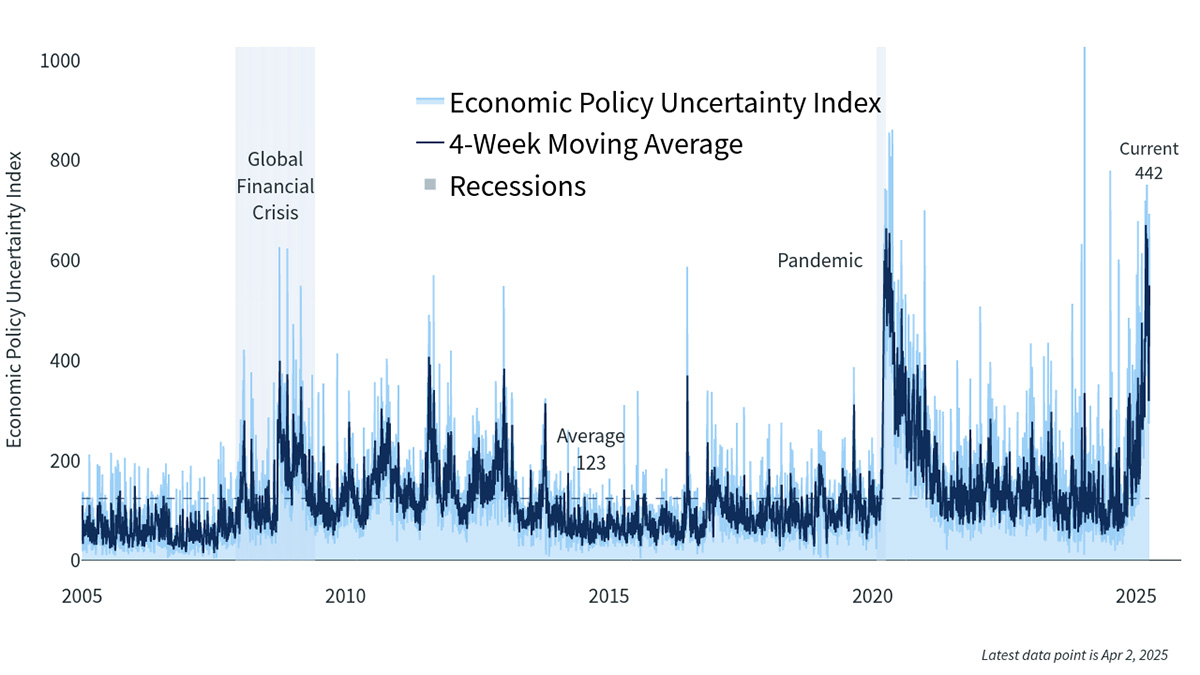

Unfortunately for investors, consumers and businesses, uncertainty is still quite high. In fact, the word “uncertainty” is showing up very frequently in earnings calls, Federal Reserve governor speeches and economic newsletters. After an onslaught of policy proposals and executive orders, it is unclear where U.S. federal policy will land on several issues. Economic data has been mixed, and there is much uncertainty about both inflation and economic growth, as it appears inflation may have stalled out at above-target levels and economic growth may be slowing enough to cause the economy to fall into a recession later this year. Additionally, the administration’s announcement of sweeping tariffs at the beginning of April caused further uncertainty and led stock markets to drop in the immediate aftermath, though it’s unclear exactly what the long-term impacts of these policies will be.

While there are certainly a few pieces of data that look weaker now than they did at the beginning of the year, there is still strength in many metrics. It could be a while before investors can separate the noise from the true underlying trend, but here are some of the important indicators to watch in the meantime.

Economic Policy Uncertainty 1

Consumers and businesses feel impacts of uncertainty

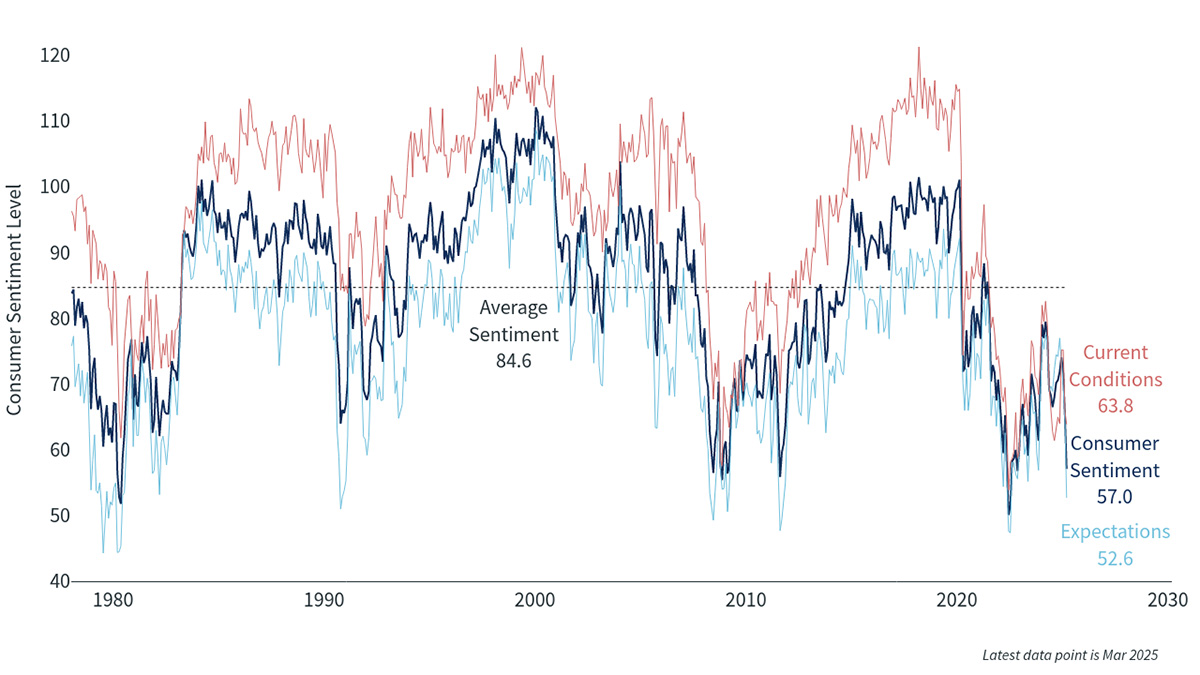

Consumer and business sentiment has been weak for the past couple of months, much of it due to the frequently changing messages about future trade policy, taxes, budget deficits and immigration, all of which could impact inflation and GDP growth. Consumers and businesses dislike uncertainty, as it makes it difficult to plan and budget, especially around long-term investments. As a result of the uncertainty, consumers and businesses may pull back from spending on both consumable and durable goods as well as services, which can harm growth and investment.

Over the past few months, consumer spending has been running below prior expectations, as uncertainty about the future weighs on household budgets. Both anecdotal evidence and economic data point to a U.S. consumer who is being more careful about how much they spend on dining out, apparel, and more expensive items like vehicles and travel. Small business sentiment has also been weaker than expected, which may result in delays to investment and hiring, which could in turn affect the labor market and lead to even less consumer spending.

Consumer Sentiment 2

If the next quarter brings more certainty around policy, businesses will be better positioned to make well-informed decisions on the costs and benefits of major projects, hiring and the design of their supply chains. Consumers will also be better able to determine how much to save and spend. It will be important to watch for changes to overall consumer and business sentiment and confidence, as they could foreshadow a slowdown, but investors shouldn’t put too much stock into any one reading.

Inflation fears continue to linger

Inflation measures have fallen a long way from their peak but have not yet reached the elusive 2% goal set by most central bankers. The last stage of getting inflation to 2% was always bound to be the hardest, though it is taking longer than many expected.

A bigger concern than the slowing rate of change is that consumer expectations of inflation have risen, as have market expectations, which could foreshadow an upcoming rise in inflation. Some of the increase in expectations is due to proposed and enacted tariffs, but also to other underlying price pressures and a weakening dollar, which makes foreign goods more expensive. If inflation expectations stay high, it could prevent the Fed from cutting rates, even if growth slows. Beyond just current inflation readings, many economists and forecasters will be watching for any changes in future inflation expectations embedded in Treasury Inflation-Protected Securities (TIPS), forward rates and consumer surveys.

No action yet from the Federal Reserve but cuts could come

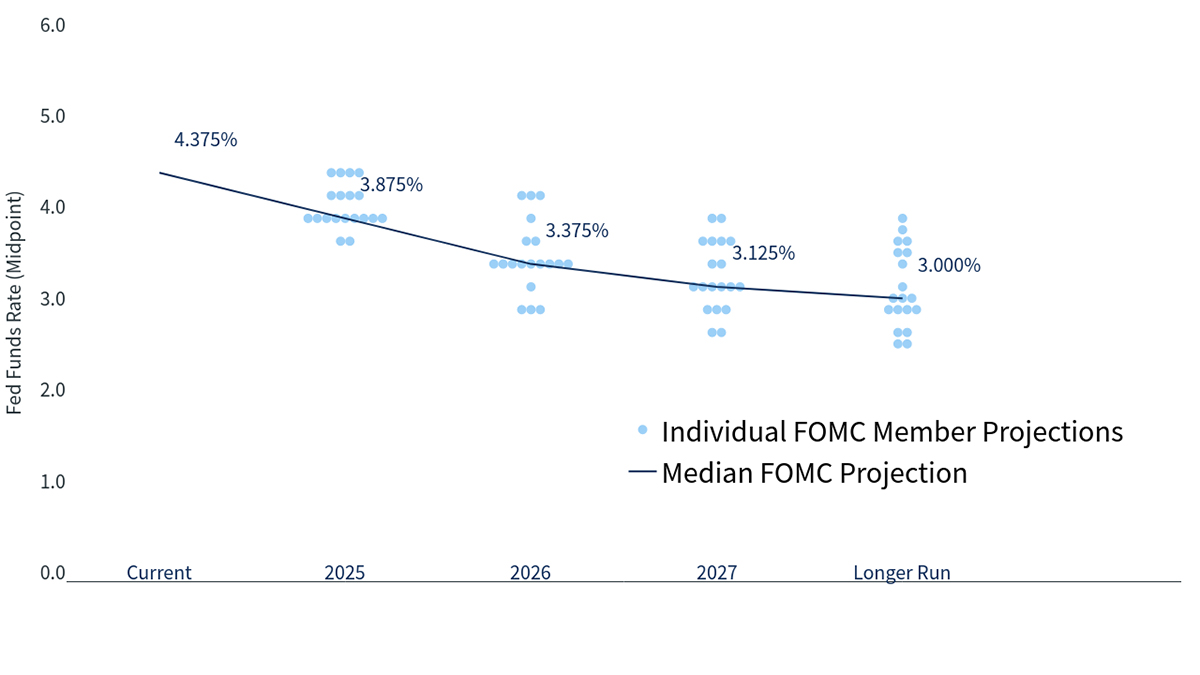

The Fed has made no moves in 2025 so far and is not expected to change rates for at least a few more months. Elevated inflation levels prevent the Fed from cutting rates just yet, but thankfully economic growth is still positive and unemployment is low enough that the Fed doesn’t have to worry yet that high rates are too restrictive. The most recent dot plot from mid-March shows that Fed governors expect to cut interest rates only two more times in 2025, unchanged from the beginning of the year, as they believe the economy will still produce modest GDP growth and inflation will remain above their 2% target for most of the year. They did lower their forecast for growth for 2025 and raised their expectations for inflation, but governors still expect positive growth for the foreseeable future and an eventual fall in inflation.

Federal Reserve Dot Plot 3

If the economy does stumble, the Fed is ready to step in to cut rates, as long as inflation is not rising. Fiscal policy may be challenged to help prop up a weakening economy given already sizeable deficits, but with the fed funds rate at 4.25-4.5%, there is plenty of monetary firepower available. The Fed’s real challenge will be if inflation is still high when growth stumbles, as their dual mandate to support full employment and stable prices could come into conflict.

Market returns sluggish to start the year

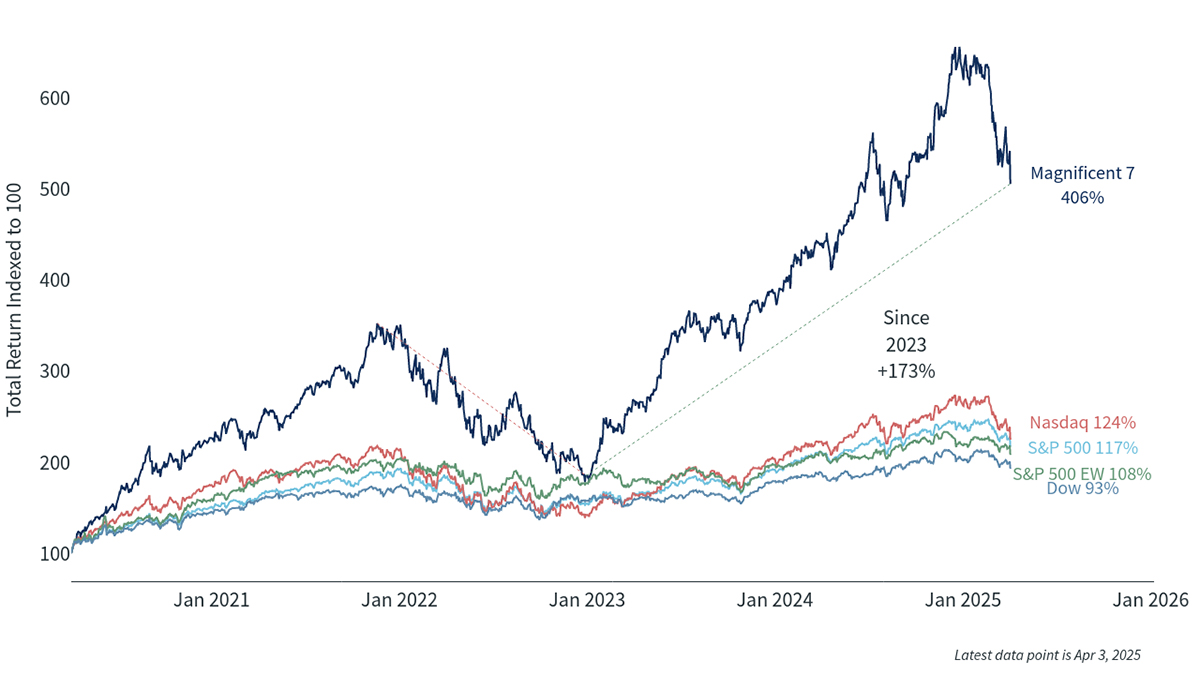

As a result of the uncertainty around where the economy and inflation are headed, stocks stumbled out of the gates in 2025 and bond yields have fallen. The S&P 500 fell4.27% in the first quarter, led by the “Magnificent 7” stocks that had propelled the market higher the prior two years, and weakened even further in the first few days of April. The 10-year Treasury finished the first quarter with a yield of only 4.21%, down 0.36% year to date. Gold, a traditional safe haven during times of uncertainty, is at record highs, trading above $3,000 per ounce during the first quarter. The U.S. dollar has weakened from the highs set in late 2024 on signs of weaker economic growth, policy uncertainty, more robust performance in other developed nations and the possibility of lower U.S. interest rates later this year.

"Magnificent 7" Stocks 4

In general, it is healthy for an equity market that has produced such strong returns the last couple of years to reset to more attractive valuations, and for more stocks and sectors to participate in the overall performance of the index. The main concern with the falling market is that it could be another reason for consumers to pull back on spending as overall wealth declines. Through the end of the first quarter, the declines of the S&P 500 and other large cap indices had only fallen into correction territory (a 10% sell off), not a bear market (greater than 20% sell off), and bonds and foreign stocks had a good quarter, so a diversified portfolio was not down much in the quarter. However, the Nasdaq entered bear territory and foreign stocks have given up most of their gains in early April, as volatility and uncertainty accelerated to start the second quarter.

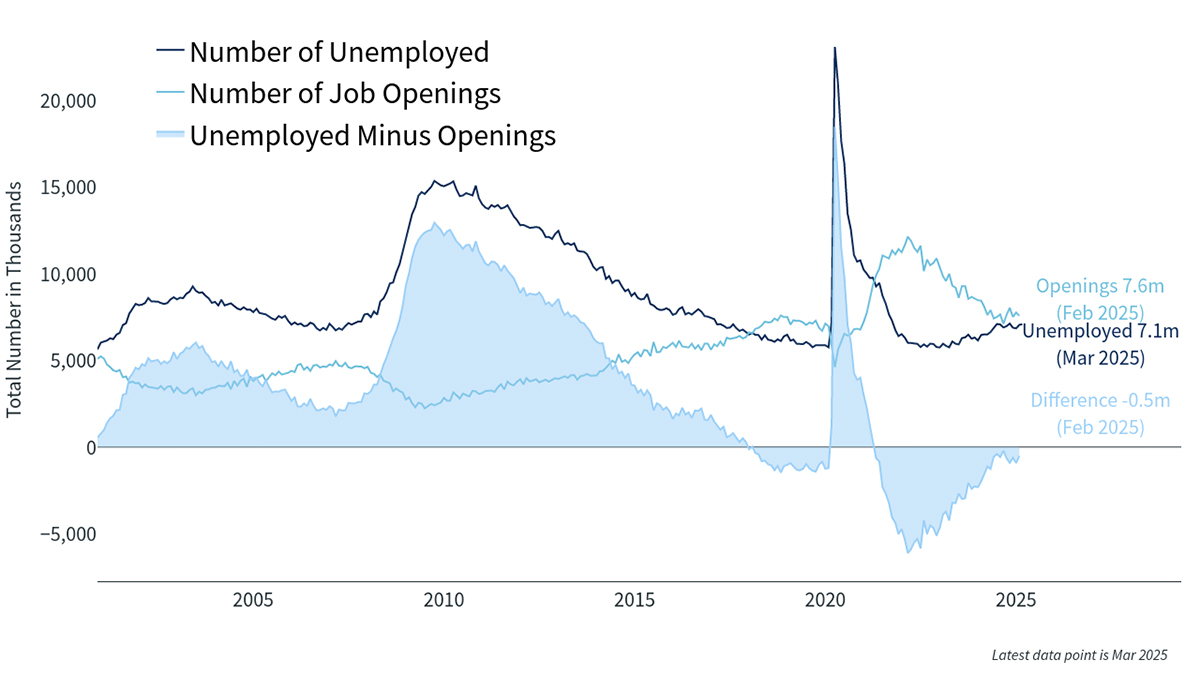

Labor markets still strong, though signs of caution exist

Despite some headwinds, unemployment remains very low. Wages are growing strongly, but not so strongly that they risk feeding into inflation. Job openings are off their highs but are in line with a solid labor market. Weekly jobless claims have stayed low, despite challenges with natural disasters and recent reductions to the federal government workforce. Productivity is growing at roughly 2% per year, allowing companies to grow profits and pay higher wages at the same time.

Unemployment and Job Openings 5

Consumer surveys do show an uptick in people who are worried about their employment and continuing claims for unemployment benefits are ticking up, implying it is more difficult to find work once a person becomes unemployed. The Job Openings and Labor Turnover Survey (JOLTS) has softened over the past year, but most measures are now in line with pre-pandemic levels, which was a still solid labor market. It will be important to see if the trend downward in openings and quits continues, and if employee concerns about their future job prospects continue to increase, as these data points can often precede future increases in the overall unemployment rate.

Looking ahead

Inflation may have stalled but it is still much lower than it was in 2022 and 2023. U.S. stock markets are lower to start the year but are up considerably over the past two years, and international developed and emerging markets stocks have had a good start to the year, reminding everyone of the importance of diversification. If the political noise dies down and there is more policy certainty, it is entirely plausible that U.S. economic growth will remain positive for the rest of the year, and that stocks recover their early losses.

Timing the market is notoriously difficult, and some of the best returns have been made during periods of uncertainty, stress or bearish sentiment. It is also true that study after study has shown that making investment decisions based on politics or out of fear of uncertainty often leads to poor performance. This means that despite the almost overwhelming news flow and daily change in policy proposals, for long-term investing success, it is almost always best to stick to an investment strategy that incorporates diversification and takes advantage of rebalancing opportunities as markets shift.

The views and opinions represented in this message are my own and do not necessarily reflect the perspective of Bremer Bank, its subsidiaries or affiliates, or its employees. This message is provided for information purposes only and nothing in it constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold any security. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor.

About Josh Howard

Josh Howard is the Chief Investment Officer at Bremer Bank. He leads Bremer’s investment team, overseeing the development, management, delivery and communication of investment strategies and model portfolios that meet the needs of Bremer Wealth clients. Josh has more than 20 years of financial services experience, and spent seven years at the Royal Bank of Canada in a variety of investment leadership roles. Most recently, he served as Director of Global Risk Management for RBC Global Asset Management, where he managed all areas of investment risk oversight, covering equities, fixed income and alternatives as well as was responsible for deriva...

More on Josh%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,35.91c.05,14.91-12.02,27.03-26.99,27.12-14.79.09-26.95-12.03-27.01-26.91-.06-15.01,11.91-27.11,26.87-27.16,14.95-.05,27.08,12,27.13,26.95ZM45.08,18.32c-2.37,0-4.6-.07-6.82.02-3.32.14-5.55,1.94-6.61,5-.51,1.46-.62,3.07-.75,4.63-.12,1.45-.03,2.91-.03,4.54h-6.14v6.98h6.16v16.82h7.5v-16.89c1.6,0,2.98.05,4.34-.03.4-.02,1.05-.36,1.11-.65.4-2.02.67-4.06,1.01-6.3h-6.51c0-1.55,0-2.92,0-4.29,0-2.53,1.12-3.72,3.67-3.83,1-.05,2,0,3.06,0v-5.97Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,36.15c-.07,14.97-12.18,26.99-27.11,26.89-14.9-.1-26.92-12.16-26.89-26.99.03-15.01,12.15-27.11,27.15-27.08,14.87.03,26.92,12.23,26.85,27.18ZM36.62,51c.03-.53.08-.98.08-1.42,0-3.11-.04-6.22.02-9.33.05-2.49,1.88-4.31,4.23-4.36,2.31-.05,3.92,1.63,4,4.27.06,1.88.02,3.77.02,5.66,0,1.72,0,3.43,0,5.17h6.01c0-5.04.18-9.98-.07-14.91-.16-3.17-3.26-5.57-6.55-5.78-2.85-.18-5.44.35-7.56,2.83-.08-1.07-.14-1.75-.19-2.46h-5.83v20.33h5.84ZM27.06,30.66h-5.99v20.32h5.99v-20.32ZM24.06,20.18c-2.03-.03-3.64,1.57-3.66,3.65-.02,2.14,1.45,3.73,3.52,3.78,2,.05,3.74-1.57,3.82-3.56.08-2.04-1.63-3.84-3.68-3.87Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M35.95,9.01c14.89-.05,27.01,12,27.05,26.9.04,14.88-12.08,27.09-26.9,27.08-14.88,0-27.08-12.13-27.1-26.93-.02-14.85,12.08-27,26.95-27.05ZM36.02,18.76c-2.54,0-5.09-.01-7.63,0-5.58.03-9.63,4.08-9.65,9.64-.01,5.09-.02,10.18,0,15.27.02,5.3,3.98,9.46,9.28,9.57,5.34.11,10.69.11,16.03,0,5.31-.11,9.22-4.26,9.24-9.58.02-5.19.03-10.38,0-15.57-.04-5.2-4.12-9.25-9.33-9.31-2.65-.03-5.29,0-7.94,0Z'/%3e%3cpath%20class='cls-1'%20d='M50.22,36.02c0,2.54.02,5.09,0,7.63-.03,3.73-2.68,6.49-6.41,6.54-5.19.06-10.37.06-15.56,0-3.7-.04-6.42-2.81-6.45-6.52-.04-5.14-.04-10.27,0-15.41.03-3.64,2.72-6.38,6.36-6.42,5.24-.06,10.48-.06,15.71,0,3.67.04,6.31,2.75,6.35,6.41.03,2.59,0,5.19,0,7.78ZM36.1,26.6c-5.11-.05-9.38,4.12-9.43,9.2-.05,5.28,4.02,9.53,9.18,9.59,5.26.07,9.54-4.07,9.66-9.35.11-5.02-4.25-9.4-9.41-9.44ZM43.25,26.81c.02,1.05,1.05,2.03,2.08,1.99,1.07-.04,2.04-1.06,1.92-2.12-.12-1.15-.78-1.84-1.98-1.87-1.13-.03-2.05.89-2.02,1.99Z'/%3e%3cpath%20class='cls-1'%20d='M42.2,36.07c-.04,3.39-2.95,6.22-6.3,6.13-3.35-.09-6.06-2.89-6.05-6.23,0-3.28,2.86-6.13,6.15-6.14,3.36,0,6.24,2.89,6.2,6.24Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M8.99,36.02c0-14.9,12.03-27.02,26.87-27.06,14.99-.03,27.2,12.17,27.15,27.13-.05,14.95-12.18,26.99-27.14,26.94-14.9-.05-26.87-12.08-26.87-27.02ZM36,48.01c4.01-.29,8.03-.5,12.03-.89,2.54-.25,3.77-1.45,4.16-3.94.75-4.76.75-9.54.02-14.3-.39-2.56-1.67-3.79-4.23-4.08-7.98-.91-15.96-.92-23.94,0-2.67.31-4.16,1.68-4.27,4.36-.18,4.57-.17,9.15,0,13.71.1,2.6,1.56,3.98,4.19,4.24,4,.4,8.01.6,12.04.89Z'/%3e%3cpath%20class='cls-1'%20d='M41.32,35.97c-2.91,1.7-5.64,3.29-8.55,4.98v-9.87c2.87,1.64,5.61,3.21,8.55,4.89Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)