It was an eventful 2024, particularly for global politics. More than 70 countries — equivalent to roughly half of the world’s voting age population — held elections. Many of these resulted in a change of party, as inflation, war and general political fatigue led many countries to oust incumbents.

These new administrations will play a key role in shaping the 2025 global economy. Economic reports that came in toward the end of last year often contained positive signs. The ways that new governments react to major issues will certainly affect how the data plays out throughout the year. Another trend to watch closely is the continued advancement of artificial intelligence, which captured public attention and propelled AI-related stocks in 2024. While the economy has yet to experience anything truly transformational from AI, the companies that produce the semiconductors and energy that power AI tools have certainly benefited.

Here's a look at some key economic data points we watched closely last year that could indicate where the next 12 months might take us.

2024 brought a strong economy and labor markets

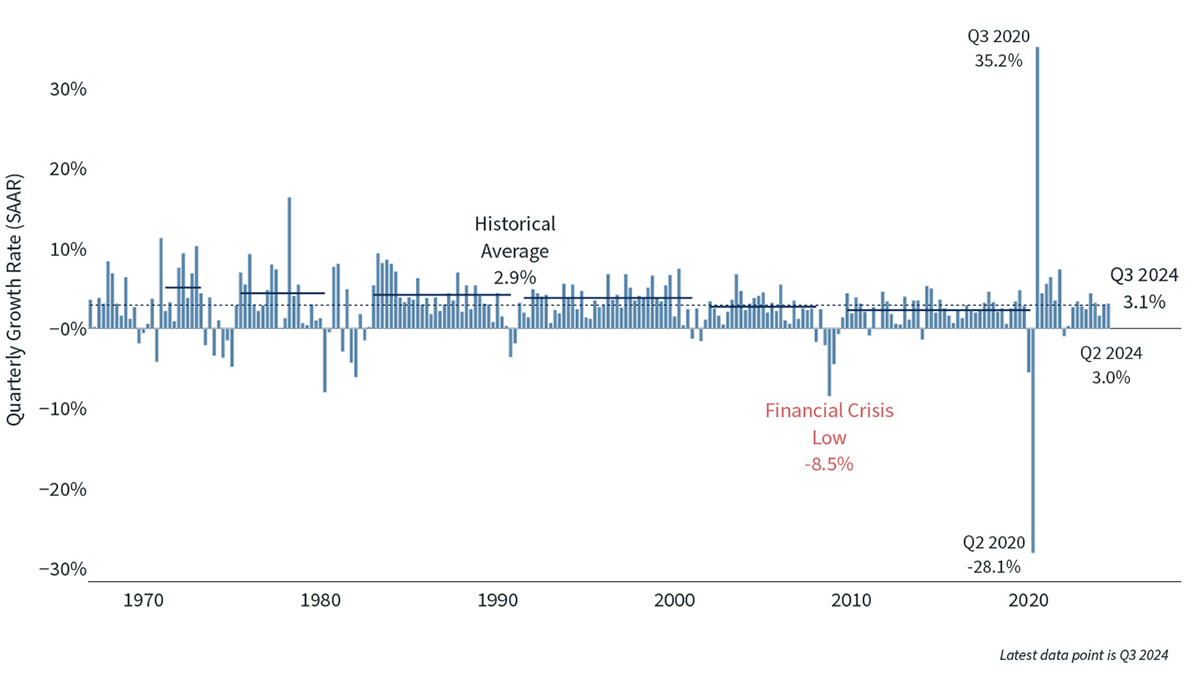

The U.S. economy experienced unexpectedly strong growth throughout 2024. Gross domestic product growth for the full year will likely finish above 2.5% once the final fourth quarter numbers are released, which is below the 2023 level but above longer-term averages, and well above what was expected coming into 2024. Much of the growth came from strong consumer spending, aided by increases in productivity and fiscal spending, with only trade deficits acting as a consistent detractor.

Productivity growth of roughly 2%, combined with nominal wage growth of around 4% and inflation levels between 2.5% and 3.5% (depending on the measure) allowed employees to experience real wage growth for the past year without denting corporate earnings. Payrolls also continued to grow at solid rates, though below the levels seen in 2023, and unemployment remained at historically low levels. Strong wage growth and a solid labor market aided consumer spending throughout the year, even with most pandemic-related stimulus funding now gone.

Gross Domestic Product1

Inflation fell, though the target rate remains elusive

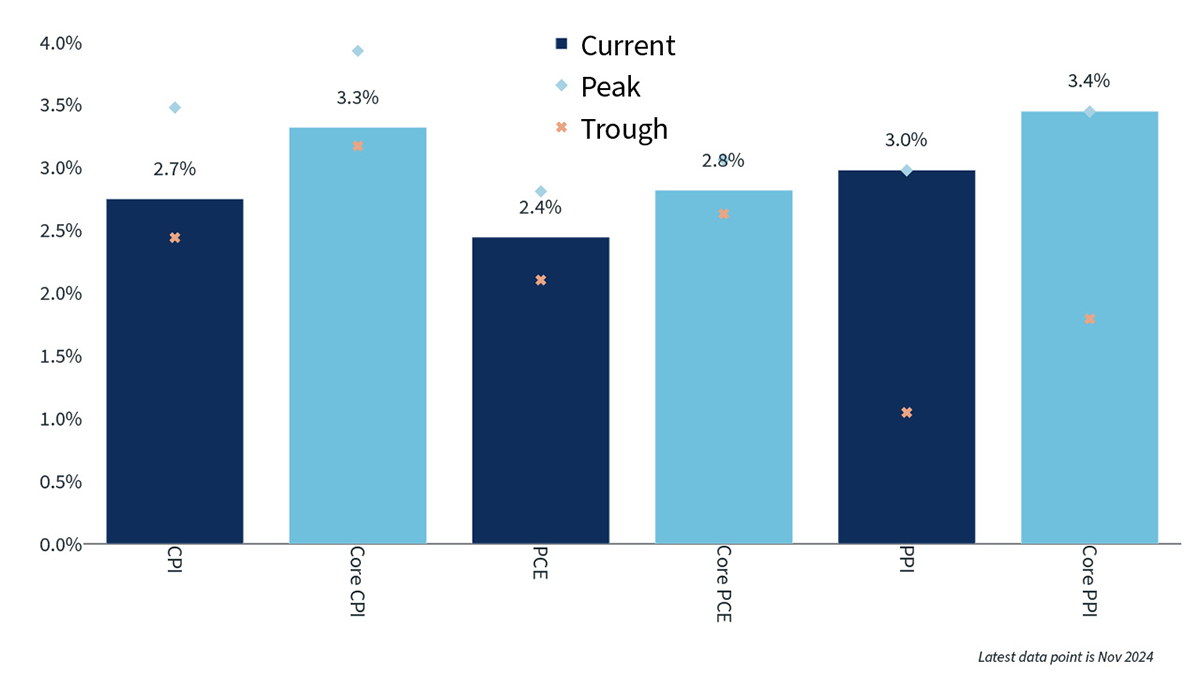

Inflation remained an important story in 2024, but less so than in prior years because it is almost back to target and is below wage growth. The headline consumer price index (CPI) in the U.S. has stayed below 4% for over a year and a half, but has not yet fallen all the way to the target rate of 2%. This is worrisome for central bankers, even if the absolute levels of inflation are not all that high. Both core and headline CPI, as well as other inflation measures, spent the second half of 2024 stuck between 2.5% and 3.5%, causing some concern that more work needs to be done in the form of higher short-term interest rates to bring inflation down to 2%.

Inflation2

Rate cuts got underway but may slow in 2025

Due to falling inflation and good-but-not-too-hot economic growth, the Federal Reserve was able to begin cutting rates in the second half of 2024. The Fed ended up cutting rates three times, totaling 100 basis points (1%), reducing the fed funds rate to a range of 4.25% to 4.5% by the end of the year. Many other central banks cut rates multiple times as well, including the Bank of England, the Bank of Canada and the European Central Bank, though the reduction amounts varied between the banks given differences in inflation levels and growth rates.

Due to concerns that inflation is stuck above 2%, as well as solid GDP growth and economic policies that may cause inflation to increase, the Fed has indicated a reluctance to cut rates much more in 2025. The latest forecast from the Fed revealed an expectation of only two, 25-basis-point cuts in 2025, much fewer than it predicted just three months earlier. As a result of this change in forecast, longer-term rates actually rose throughout the fourth quarter of 2024 despite the cuts to short-term rates. This caused the 10-year Treasury yield to rise almost a full percentage point from its low to finish the year with a yield of 4.58%.

Stocks and bonds were buoyed by other strong indicators

It maybe isn’t much of a surprise that in a year with surprisingly strong GDP growth and falling short-term interest rates, stocks had a very good year, though bonds barely eked out a positive return. The S&P 500 finished the year with a total return of 25%, as U.S. large-cap stocks, especially the so-called “Magnificent 7,” were the big winners once again, having been on a tear for two straight years. The Russell 2000 Index of small-cap U.S. stocks had a good year as well, producing a total return of 11%, and international developed stocks were up 4%, but both greatly lagged the S&P 500. The Bloomberg U.S. Aggregate Bond Index produced a total return of only 1.3%, slightly below the 1.9% return in 2023, but U.S. high-yield bonds had a nice year, producing a total return of 8%.

After two straight years of 20% or greater returns on the S&P 500, equity valuations are a bit stretched, especially for U.S. large-cap companies. There are plenty of pockets of value, however, including in U.S. small-cap and non-U.S. equities. Credit spreads are very tight in both investment-grade and high-yield bonds, but absolute yields are still attractive relative to the past decade.

Stock and Bond Returns3

Looking ahead

The start of every year is oftentimes accompanied by uncertainty in how the economy will play out. For example, one year ago, few people forecasted that the S&P 500 would produce a second consecutive year with a total return above 20%, nor did many predict that GDP growth would be over 2.5% or that long-term Treasury yields would rise after the Fed started cutting interest rates in the second half of 2024.

The start to 2025 is no different. It is difficult to predict how quickly inflation will fall to 2%, or even dismiss the idea that inflation may rise due to trade, immigration and fiscal policy. The fed funds rate could be cut another 1%, or GDP growth and inflation may be strong enough to cause the Fed to keep short-term rates where they are for the entire year. If the Fed does cut rates, it does not necessarily mean that mortgage rates or other borrowing costs will fall, or that the stock market will automatically go up, as the market may have already incorporated those actions into the current price.

There will certainly be surprises in economic data, government policy and geopolitical actions in 2025, both good and bad. With new governments in several countries enacting new policies, there will be many existing policy proposals that are not adopted, or are modified in significant ways, so it is best to not overreact to every headline or pronouncement. For almost all investors, the focus should remain on maintaining diversified portfolios and avoiding the temptation to time the market.

About Josh Howard

Josh Howard is the Chief Investment Officer at Bremer Bank. He leads Bremer’s investment team, overseeing the development, management, delivery and communication of investment strategies and model portfolios that meet the needs of Bremer Wealth clients. Josh has more than 20 years of financial services experience, and spent seven years at the Royal Bank of Canada in a variety of investment leadership roles. Most recently, he served as Director of Global Risk Management for RBC Global Asset Management, where he managed all areas of investment risk oversight, covering equities, fixed income and alternatives as well as was responsible for deriva...

More on Josh%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,35.91c.05,14.91-12.02,27.03-26.99,27.12-14.79.09-26.95-12.03-27.01-26.91-.06-15.01,11.91-27.11,26.87-27.16,14.95-.05,27.08,12,27.13,26.95ZM45.08,18.32c-2.37,0-4.6-.07-6.82.02-3.32.14-5.55,1.94-6.61,5-.51,1.46-.62,3.07-.75,4.63-.12,1.45-.03,2.91-.03,4.54h-6.14v6.98h6.16v16.82h7.5v-16.89c1.6,0,2.98.05,4.34-.03.4-.02,1.05-.36,1.11-.65.4-2.02.67-4.06,1.01-6.3h-6.51c0-1.55,0-2.92,0-4.29,0-2.53,1.12-3.72,3.67-3.83,1-.05,2,0,3.06,0v-5.97Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,36.15c-.07,14.97-12.18,26.99-27.11,26.89-14.9-.1-26.92-12.16-26.89-26.99.03-15.01,12.15-27.11,27.15-27.08,14.87.03,26.92,12.23,26.85,27.18ZM36.62,51c.03-.53.08-.98.08-1.42,0-3.11-.04-6.22.02-9.33.05-2.49,1.88-4.31,4.23-4.36,2.31-.05,3.92,1.63,4,4.27.06,1.88.02,3.77.02,5.66,0,1.72,0,3.43,0,5.17h6.01c0-5.04.18-9.98-.07-14.91-.16-3.17-3.26-5.57-6.55-5.78-2.85-.18-5.44.35-7.56,2.83-.08-1.07-.14-1.75-.19-2.46h-5.83v20.33h5.84ZM27.06,30.66h-5.99v20.32h5.99v-20.32ZM24.06,20.18c-2.03-.03-3.64,1.57-3.66,3.65-.02,2.14,1.45,3.73,3.52,3.78,2,.05,3.74-1.57,3.82-3.56.08-2.04-1.63-3.84-3.68-3.87Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M35.95,9.01c14.89-.05,27.01,12,27.05,26.9.04,14.88-12.08,27.09-26.9,27.08-14.88,0-27.08-12.13-27.1-26.93-.02-14.85,12.08-27,26.95-27.05ZM36.02,18.76c-2.54,0-5.09-.01-7.63,0-5.58.03-9.63,4.08-9.65,9.64-.01,5.09-.02,10.18,0,15.27.02,5.3,3.98,9.46,9.28,9.57,5.34.11,10.69.11,16.03,0,5.31-.11,9.22-4.26,9.24-9.58.02-5.19.03-10.38,0-15.57-.04-5.2-4.12-9.25-9.33-9.31-2.65-.03-5.29,0-7.94,0Z'/%3e%3cpath%20class='cls-1'%20d='M50.22,36.02c0,2.54.02,5.09,0,7.63-.03,3.73-2.68,6.49-6.41,6.54-5.19.06-10.37.06-15.56,0-3.7-.04-6.42-2.81-6.45-6.52-.04-5.14-.04-10.27,0-15.41.03-3.64,2.72-6.38,6.36-6.42,5.24-.06,10.48-.06,15.71,0,3.67.04,6.31,2.75,6.35,6.41.03,2.59,0,5.19,0,7.78ZM36.1,26.6c-5.11-.05-9.38,4.12-9.43,9.2-.05,5.28,4.02,9.53,9.18,9.59,5.26.07,9.54-4.07,9.66-9.35.11-5.02-4.25-9.4-9.41-9.44ZM43.25,26.81c.02,1.05,1.05,2.03,2.08,1.99,1.07-.04,2.04-1.06,1.92-2.12-.12-1.15-.78-1.84-1.98-1.87-1.13-.03-2.05.89-2.02,1.99Z'/%3e%3cpath%20class='cls-1'%20d='M42.2,36.07c-.04,3.39-2.95,6.22-6.3,6.13-3.35-.09-6.06-2.89-6.05-6.23,0-3.28,2.86-6.13,6.15-6.14,3.36,0,6.24,2.89,6.2,6.24Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M8.99,36.02c0-14.9,12.03-27.02,26.87-27.06,14.99-.03,27.2,12.17,27.15,27.13-.05,14.95-12.18,26.99-27.14,26.94-14.9-.05-26.87-12.08-26.87-27.02ZM36,48.01c4.01-.29,8.03-.5,12.03-.89,2.54-.25,3.77-1.45,4.16-3.94.75-4.76.75-9.54.02-14.3-.39-2.56-1.67-3.79-4.23-4.08-7.98-.91-15.96-.92-23.94,0-2.67.31-4.16,1.68-4.27,4.36-.18,4.57-.17,9.15,0,13.71.1,2.6,1.56,3.98,4.19,4.24,4,.4,8.01.6,12.04.89Z'/%3e%3cpath%20class='cls-1'%20d='M41.32,35.97c-2.91,1.7-5.64,3.29-8.55,4.98v-9.87c2.87,1.64,5.61,3.21,8.55,4.89Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)